Last Updated on Nov 8, 2020

People can always find a use for money, so it costs to borrow money. Interest may be defined as the charge for using the borrowed money. It is an expense for the person who borrows money and income for the person who lends money. Interest is charged on principal amount at a certain rate for a certain period. For example, 10% per year, 4% per quarter or 2% per month etc. Principal amount means the amount of money that is originally borrowed from an individual or a financial institution. It does not include interest. In practice, the interest is charged using one of two methods. These are:

- Simple interest method

- Compound interest method

These methods are briefly explained below:

Simple Interest method:

Under this method, the interest is charged only on the amount originally lent (principal amount) to the borrower. Interest is not charged on any accumulated interest under this method. Simple interest is usually charged on short-term borrowings.

Simple interest formula:

Simple interest can be easily computed using the following formula:

Simple Interest = PTR / 100

Where;

I = Simple interest

P = Principal amount

R = rate of interest

T = number of periods

Example 1:

A loan of Rs. 10,000 has been issued for 6-years. Compute the amount to be repaid to the lender if simple interest is charged at 5% per year.

Solution:

P =Rs. 1,000; i = 5%; n = 5

By putting the values of P, i and n into the simple interest formula:

=Rs. 10,000 × 5% × 6

=Rs. 10,000 × .05 × 6

=Rs. 3,000

At the end of sixth year, the amount of Rs.13,000 (Rs. 10,000 principal +Rs. 3,000 accumulated interest) will be repaid to the lender.

Compound interest method:

Compounding of interest is very common. Under this method, the interest is charged on principal plus accumulated interest. The amount of interest for a period is added to the amount of principal to compute the interest for next period. In other words, the interest is reinvested to earn more interest. The interest may be compounded monthly, quarterly, semiannually or annually. Consider the following example to understand the whole procedure of compounding.

Example 2:

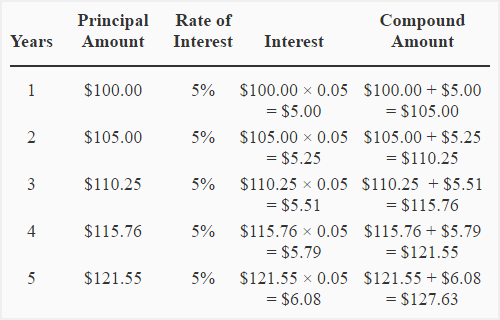

Suppose, you have deposited Rs. 100 with a bank for five years at a rate of 5% per year compounded annually. The interest for the first year will be computed on Rs. 100 and you will have Rs. 105 (Rs. 100 principal +Rs. 5 interest) at the end of first year. The interest for the second year will be computed on Rs. 105 and at the end of second year you will have Rs. 110.25 (Rs. 105 principal + 5.25 interest). The interest for the third year will be computed on Rs. 110.25 and at the end of third year you will have Rs. 115.76 (110.25 principal + 5.51 interest). The following table shows the computation for 5-year period of investment.

Under the compound interest system, when interest is added to the principal amount, the resulting figure is known as the compound amount. In the above table, the compound amount at the end of each year has been computed in the last column. Notice that the compound amount at the end of a year becomes the principal amount to compute the interest for the next year.

Compound amount formula:

The above procedure of computing compound amount is lengthy and time-consuming. Fortunately, a formula is available to compute compound amount for any number of periods. It is given below:

Where;

S = compound amount

P = Principal amount

i = rate of interest

n = number of periods

Now we would compute the compound amount in above example using compound amount formula:

=Rs. 100 × (1 + 5%)5

=Rs. 100 × (1 + .05)5

=Rs. 100 × (1.05)5

=Rs. 100 × 1.276

=Rs. 127.6

Once the compound amount has been computed, the amount of interest earned over the investment period can be computed by subtracting principal amount from the compound amount. It is shown below:

Interest earned over a 5-year period: Rs. 127.6 –Rs. 100 =Rs. 27.6

Compound interest is greater than simple interest:

Compound interest is greater than simple interest. The reason is very simple. Under simple interest system, the interest is computed only on principal amount whereas, under compound interest system, the interest is computed on principle as well as on accumulated interest. Consider the following example for the explanation of this point:

Example 3:

A woman has deposited Rs. 6,000 in a saving account. Bank pays interest at a rate of 9% per year.

Required: Compute the amount of interest that will be earned over a 12-year period:

- if the interest is simple?

- if the interest is compounded annually?

Solution:

(1) Simple interest:

=Rs. 6,000 × 0.09 × 12

=Rs. 6,480

(2) Compound interest:

=Rs. 6,000 × (1 + 9%)12

=Rs. 6,000 × 2.813*

=Rs. 16,878

Interest:Rs. 16878 –Rs. 6,000 =Rs. 10,878

Notice that compound interest is more than simple interest by Rs. 4,398 (Rs. 10,878 –Rs. 6,480).

Summary

In this blog post, we have explained the Concept of Simple and Compound Interest in detail. We have taken some examples which are also explained in depth to clarify the concept in the student’s mind. We hope you like our blog. Check here for related posts. And, do not forget to share your views in the comment section below.